Insurance Coverage Explained

Full Coverage vs Liability Insurance — Which One Should You Choose?

Full coverage vs liability insurance is one of the most financially significant decisions you make as a driver. Here is what each really covers and how to choose.

By Daniel Reyes · May 17, 2026 · 14 min read

Walk into any car insurance conversation and you will hear two terms more than any others: full coverage and liability insurance. Most drivers have a vague sense that full coverage costs more and covers more, and that liability is the cheaper basic option.

But very few drivers actually understand what the difference means in real dollar terms — until they file a claim and discover that their coverage did not protect them the way they thought it would.

The truth is that the choice between full coverage and liability insurance is one of the most financially significant decisions you make as a driver. Choose the wrong option for your situation and you could either be dramatically overpaying for coverage you do not need, or leaving yourself exposed to tens of thousands of dollars in out-of-pocket costs after an accident.

This guide breaks down exactly what full coverage and liability insurance include, what each one does and does not cover, and the specific factors that should drive your decision.

What Is Liability Insurance?

Liability insurance is the most basic form of car insurance and is required by law in almost every U.S. state. It covers the costs you are legally responsible for when you cause an accident — but it does not cover anything that happens to you or your own vehicle.

Liability insurance has two main components:

Bodily Injury Liability

This covers medical expenses, lost wages, pain and suffering, and legal fees for other people who are injured in an accident that you caused. It does not cover your own injuries. Bodily injury liability limits are typically expressed as two numbers such as 25/50, meaning $25,000 per injured person and $50,000 maximum per accident.

Property Damage Liability

This covers the cost of repairing or replacing other people's vehicles and property that you damage in an accident you caused. It does not cover damage to your own vehicle. Property damage liability limits are expressed as a single number such as $25,000 per accident.

State Minimum Liability Requirements

Every state sets its own minimum liability insurance requirements. For example:

- California requires 15/30/5 — $15,000 per person, $30,000 per accident bodily injury, $5,000 property damage

- Texas requires 30/60/25 — $30,000 per person, $60,000 per accident bodily injury, $25,000 property damage

- Florida requires 10/20/10 — $10,000 per person, $20,000 per accident bodily injury, $10,000 property damage

These minimums are often far too low to cover the actual costs of a serious accident. If you cause an accident that exceeds your liability limits, you are personally responsible for the difference — which can mean lawsuits, wage garnishment, and asset seizure.

What Is Full Coverage Insurance?

Full coverage is not actually a single type of insurance policy. It is an industry term for a combination of coverages that together provide comprehensive protection for both your liability to others and damage to your own vehicle.

Full coverage typically includes:

Liability Insurance

The same bodily injury and property damage liability coverage described above — just with higher recommended limits than the state minimum.

Collision Coverage

Collision coverage pays for damage to your own vehicle when you are involved in a collision with another vehicle or object, regardless of who is at fault. If you rear-end another car, hit a guardrail, or roll your vehicle, collision coverage pays for your repairs minus your deductible.

Comprehensive Coverage

Comprehensive coverage pays for damage to your vehicle from non-collision events including theft, vandalism, fire, flooding, hail, fallen trees, animal strikes, and natural disasters. If a hailstorm destroys your car or your vehicle is stolen, comprehensive coverage pays for the repair or replacement minus your deductible.

Additional Coverages Often Included

Many full coverage policies also include:

- Uninsured and underinsured motorist coverage

- Medical payments coverage or personal injury protection

- Roadside assistance

- Rental car reimbursement

What Full Coverage Does NOT Cover

Despite the name, full coverage does not cover everything. Understanding the gaps is just as important as understanding what is included.

Your Own Medical Expenses

Standard full coverage does not automatically pay your medical bills after an accident. You need medical payments coverage or personal injury protection for that — which may or may not be included depending on your state and policy.

Mechanical Breakdown

If your engine fails or your transmission gives out due to normal wear and tear, full coverage does not apply. This is not an insurance event — it is a maintenance issue.

Custom Parts and Accessories

Aftermarket modifications, custom paint jobs, and non-factory accessories are typically not covered under standard full coverage unless you add specific endorsements.

Rideshare Driving

If you drive for Uber or Lyft, your personal full coverage policy typically does not cover accidents that occur while you are transporting passengers for hire. You need rideshare-specific coverage for that.

Intentional Damage

No insurance policy covers damage you cause intentionally.

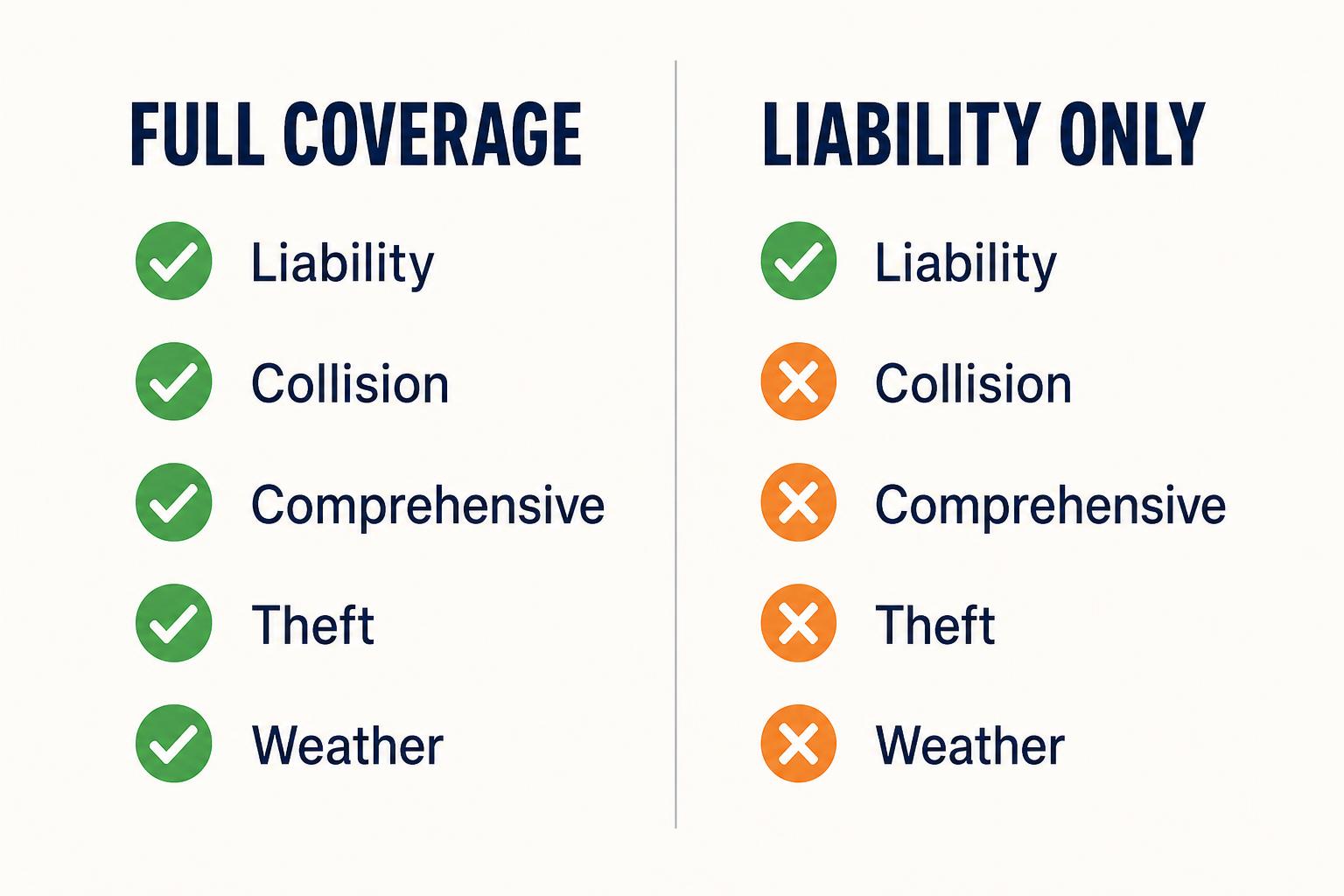

Full Coverage vs Liability — Side by Side Comparison

| Coverage | Liability Only | Full Coverage |

|---|---|---|

| Damage you cause to other vehicles | ✅ | ✅ |

| Injuries you cause to others | ✅ | ✅ |

| Damage to your own vehicle from collision | ❌ | ✅ |

| Theft of your vehicle | ❌ | ✅ |

| Weather damage to your vehicle | ❌ | ✅ |

| Vandalism to your vehicle | ❌ | ✅ |

| Uninsured motorist protection | ❌ | Often ✅ |

| Monthly premium | Lower | Higher |

How Much More Does Full Coverage Cost?

The cost difference between liability only and full coverage varies significantly based on your location, vehicle, driving history, and the coverage limits you choose. However, as a general guideline:

- The national average cost of liability only coverage is approximately $600 to $800 per year

- The national average cost of full coverage is approximately $1,500 to $2,000 per year

- The difference is typically $700 to $1,200 per year depending on your situation

That additional cost buys you protection for your own vehicle — which for many drivers represents their most valuable asset after their home.

7 Key Factors to Help You Decide

Factor 1 — Do You Have a Car Loan or Lease?

If you are financing or leasing your vehicle, you almost certainly do not have a choice. Lenders and leasing companies require full coverage as a condition of the loan or lease agreement. They need to protect their financial interest in the vehicle. If you drop to liability only while carrying a loan or lease, you are violating your contract and could face serious consequences.

Factor 2 — How Much Is Your Vehicle Worth?

This is the most important factor for drivers who own their vehicle outright. The general rule of thumb used by financial advisors is:

If your annual collision and comprehensive premium exceeds 10% of your vehicle's current market value, dropping to liability only may make financial sense.

For example:

- Vehicle value: $6,000 · Annual collision and comprehensive premium: $800 · $800 ÷ $6,000 = 13.3% — above the 10% threshold → Consider dropping to liability only

- Vehicle value: $20,000 · Annual collision and comprehensive premium: $900 · $900 ÷ $20,000 = 4.5% — well below the 10% threshold → Full coverage makes strong financial sense

For a deeper breakdown of how deductibles change this math, see our guide to car insurance deductibles explained.

Factor 3 — Could You Afford to Replace Your Vehicle Out of Pocket?

Ask yourself honestly: if your car was totaled tomorrow, could you afford to replace it without an insurance payout? If the answer is no — and for most drivers it is — full coverage provides essential financial protection. The monthly premium cost is far smaller than the financial shock of losing a vehicle you cannot replace.

Factor 4 — Where Do You Live and Park?

Your location significantly affects the risk profile of your vehicle. If you live in an area with high rates of vehicle theft, vandalism, flooding, hail storms, or wildfires, comprehensive coverage becomes substantially more valuable. If you regularly park in high-traffic urban areas where the risk of collision damage is elevated, collision coverage provides important protection.

Factor 5 — What Is Your Driving History?

Drivers with a history of accidents or traffic violations face a higher statistical probability of future claims. For these drivers, the protection of full coverage is more likely to be used and therefore more valuable. Conversely, drivers with a long history of clean driving may reasonably assess their collision risk as lower and factor that into their coverage decision — though nobody can predict accidents with certainty.

Factor 6 — How Much Are Your Savings?

Full coverage with a high deductible is a common middle ground for drivers with solid emergency savings. By choosing a $1,000 or $1,500 deductible, you reduce your full coverage premium significantly while maintaining protection against catastrophic losses. If you have limited savings and could not cover a $1,000 deductible comfortably, a lower deductible provides important protection — but increases your premium.

Factor 7 — How Much Do You Drive?

Drivers who commute long distances or spend significant time on busy highways face more exposure to accident risk than drivers who use their vehicle only occasionally. Higher mileage and more driving time statistically increase the probability of a collision, which increases the value of collision coverage.

What About State Minimum Liability Limits — Are They Enough?

For most drivers the answer is a clear no. State minimum liability limits were set decades ago and have not kept pace with the actual costs of modern accidents.

Consider this scenario: you cause an accident that results in $150,000 in medical bills for the other driver, who is seriously injured. If you carry California's minimum liability of $15,000 per person, you are personally responsible for the remaining $135,000. Your wages can be garnished. Your bank accounts can be levied. Your assets can be seized.

Most insurance professionals recommend carrying at least:

- $100,000 per person in bodily injury liability

- $300,000 per accident in bodily injury liability

- $100,000 in property damage liability

These higher limits typically add only $100 to $200 per year to your premium — a small price for dramatically greater financial protection. It is also worth pairing these higher limits with uninsured motorist coverage, because the very drivers most likely to hit you are the ones least likely to carry adequate insurance themselves.

The Smart Middle Ground — What Many Experienced Drivers Choose

Many experienced drivers who own older vehicles outright choose a middle path that balances cost and protection:

- Drop collision coverage on vehicles worth less than $8,000 to $10,000

- Keep comprehensive coverage even on older vehicles since it is relatively inexpensive and covers theft, weather, and vandalism

- Carry high liability limits — $100,000/$300,000 or higher

- Add uninsured and underinsured motorist coverage

- Keep medical payments coverage or personal injury protection

This approach significantly reduces premiums compared to full coverage while maintaining protection against the most financially devastating scenarios — being sued for a serious accident you caused, or having your vehicle stolen or destroyed by weather.

Real World Example — The Cost of Choosing Liability Only

Consider David, a 35-year-old driver in Texas who owns a three-year-old Toyota Camry worth $22,000 outright. He switches from full coverage to liability only to save $900 per year.

Six months later, David falls asleep at the wheel and runs his Camry into a guardrail at highway speed. The vehicle is totaled.

Because David only has liability insurance, his own vehicle damage is not covered. He receives nothing from his insurance company for the loss of his $22,000 car.

To get back on the road, David takes out a $15,000 personal loan at 9% interest to purchase a replacement vehicle. Over five years of loan payments, he pays approximately $4,000 in interest — more than four times what he saved by dropping full coverage.

Meanwhile if David had kept full coverage with a $1,000 deductible, his insurance would have paid him approximately $21,000 for his totaled vehicle. His net premium savings of $900 for six months would have been far outweighed by the $22,000 loss. If his insurer had initially undervalued the total loss, he would have had grounds to push back — see our guide on how to fight a denied car insurance claim for the appeal playbook.

Key Takeaways

- Liability insurance only covers damage and injuries you cause to others — it does not cover your own vehicle or injuries

- Full coverage adds collision and comprehensive protection for your own vehicle on top of liability coverage

- If you have a car loan or lease, full coverage is required — you do not have a choice

- The 10% rule helps determine when dropping collision coverage makes financial sense on older vehicles

- State minimum liability limits are almost always too low — consider carrying at least $100,000/$300,000

- Comprehensive coverage is relatively inexpensive and worth keeping even on older vehicles

- The true cost of going without full coverage only becomes clear after an accident makes you wish you had it

Conclusion

The choice between full coverage and liability insurance is not simply a question of how much you want to spend on insurance. It is a question of how much financial risk you are willing and able to absorb if an accident happens.

For drivers with newer or higher-value vehicles, outstanding loans or leases, or limited emergency savings, full coverage provides essential protection that is worth every dollar of the premium difference.

For drivers who own older lower-value vehicles outright and have the savings to absorb a vehicle loss, dropping collision coverage while maintaining strong liability limits and comprehensive coverage can be a smart financial decision.

Whichever you choose, make sure your decision is based on a clear understanding of what each coverage does — and what it leaves you responsible for when you need it most.

Frequently asked questions

Is full coverage worth it for an older car?+

It depends on the vehicle's value. If your annual collision and comprehensive premium exceeds 10% of your car's current market value, dropping those coverages may make financial sense. However, always keep liability coverage and consider keeping comprehensive since it is typically inexpensive and covers theft and weather damage.

What happens if I only have liability insurance and someone hits me?+

If the other driver is at fault and has liability insurance, their policy should cover your vehicle repairs and injuries. However, if the other driver is uninsured or flees the scene, you have no coverage for your own vehicle under liability only. This is a strong argument for adding uninsured motorist coverage even if you drop collision.

Can I switch between full coverage and liability during my policy term?+

Yes, you can typically adjust your coverage at any time. However, if you have a loan or lease on your vehicle, your lender requires full coverage and removing it violates your loan agreement. Always check your loan terms before making coverage changes.

How do I know if I am paying too much for full coverage?+

Compare quotes from at least three insurers every 12 to 24 months. Premiums vary significantly between companies for identical coverage. Also review whether your deductible is set at the right level — raising your deductible from $500 to $1,000 can reduce your collision and comprehensive premium by 10% to 20%.

Continue reading

Sources

Have you ever filed a car insurance claim?

Share your experience or send us a tip — our reporters read every email and use anonymized stories to shape future coverage.

Send us your storyMore from Crash & Cover

Car Insurance Deductibles Explained — How to Choose the Right Amount

Your deductible is one of the most important decisions in your car insurance policy. Learn how deductibles work, how they affect your premium, and how to choose the right amount for your situation.

Daniel Reyes · May 16, 2026 · 10 min

Uninsured Motorist Coverage Explained — What Happens When They Have No Insurance

Roughly 1 in 8 US drivers has no insurance. Here is exactly how uninsured motorist coverage protects you, what it pays for, and how to file a claim when the at-fault driver has no policy.

Daniel Reyes · May 14, 2026 · 11 min

Liability vs Full Coverage: What Each Auto Insurance Type Actually Pays For

'Full coverage' is a marketing phrase, not a policy. Here is what liability, collision, and comprehensive really pay for.

Eve Lambert · Apr 28, 2026 · 13 min