Legal Rights & Advice

How to Fight a Denied Car Insurance Claim and Actually Win

A claim denial is not the end — it's an opening position. Here's the step-by-step playbook for appealing a denied car insurance claim and actually winning.

By Maya Doroshenko · May 15, 2026 · 14 min read

You filed your car insurance claim, submitted all the paperwork, waited patiently — and then the letter arrived. Claim denied.

For many accident victims, a claim denial feels like the end of the road. The insurance company has spoken, and there is nothing left to do but accept the decision and move on.

That could not be further from the truth.

Insurance claim denials are not final decisions. They are opening positions. Insurance companies deny claims for many reasons — some legitimate, some not — and a significant percentage of denied claims are successfully overturned on appeal when the policyholder knows the right steps to take.

In this guide, we walk you through exactly why car insurance claims get denied, how to appeal a denial effectively, and the proven strategies that give you the best chance of winning your appeal and getting the compensation you deserve.

Why Do Car Insurance Claims Get Denied?

Understanding why your claim was denied is the essential first step in fighting back. Insurance companies are required by law to provide a written explanation for every claim denial. Read it carefully — the reason given will determine your strategy for appeal.

Policy Exclusions

Every insurance policy contains exclusions — specific situations or circumstances that are not covered. Common exclusions include using your personal vehicle for commercial purposes, damage caused by mechanical failure rather than an accident, or accidents that occurred while driving under the influence.

Lapsed or Inactive Policy

If your premium payment was late or your policy lapsed before the accident occurred, the insurance company may deny your claim on the grounds that you had no active coverage at the time of the accident.

Late Reporting

Most insurance policies require you to report accidents promptly — often within 24 to 72 hours. If you delayed reporting the accident, the insurance company may use this as grounds for denial, arguing that the delay prejudiced their ability to investigate.

Disputed Liability

If the insurance company determines that you were at fault for the accident, or that fault is unclear, they may deny your claim entirely or reduce your payout based on your percentage of fault.

Insufficient Documentation

Insurance companies require specific documentation to process claims. If you did not provide adequate evidence — photographs, a police report, medical records, or repair estimates — the claim may be denied on the grounds of insufficient proof.

Pre-existing Damage

If the insurance company's adjuster determines that some or all of the damage to your vehicle existed before the accident, they may deny the portion of your claim related to that damage.

Fraud Suspicion

If the insurance company suspects that the accident was staged or that the claim involves fraud, they will deny the claim and may refer the matter for investigation.

Coverage Disputes

Sometimes insurance companies deny claims by arguing that the specific type of damage or injury you suffered is not covered under your policy, even when you believe it should be.

Step 1 — Read the Denial Letter Carefully

Your denial letter is the foundation of your appeal. Read every word carefully and identify the specific reason or reasons given for the denial.

Pay attention to:

- The exact policy provision or exclusion cited

- Any deadlines mentioned for filing an appeal

- The name and contact information of the adjuster or claims supervisor

- Any documentation the company says is missing or insufficient

Keep this letter in a safe place — you will refer to it throughout the appeals process.

Step 2 — Review Your Insurance Policy

Pull out your full insurance policy document and read the sections relevant to your denial. Insurance policies are dense and full of technical language, but understanding exactly what your policy says is critical.

Look for:

- The specific exclusion or provision cited in the denial letter

- The definitions section — insurance policies often define terms in ways that differ from everyday usage

- Your appeal rights and any deadlines for filing

- The claims procedures section

If you find that the denial letter misapplied or misinterpreted your policy language, this is one of the strongest grounds for a successful appeal.

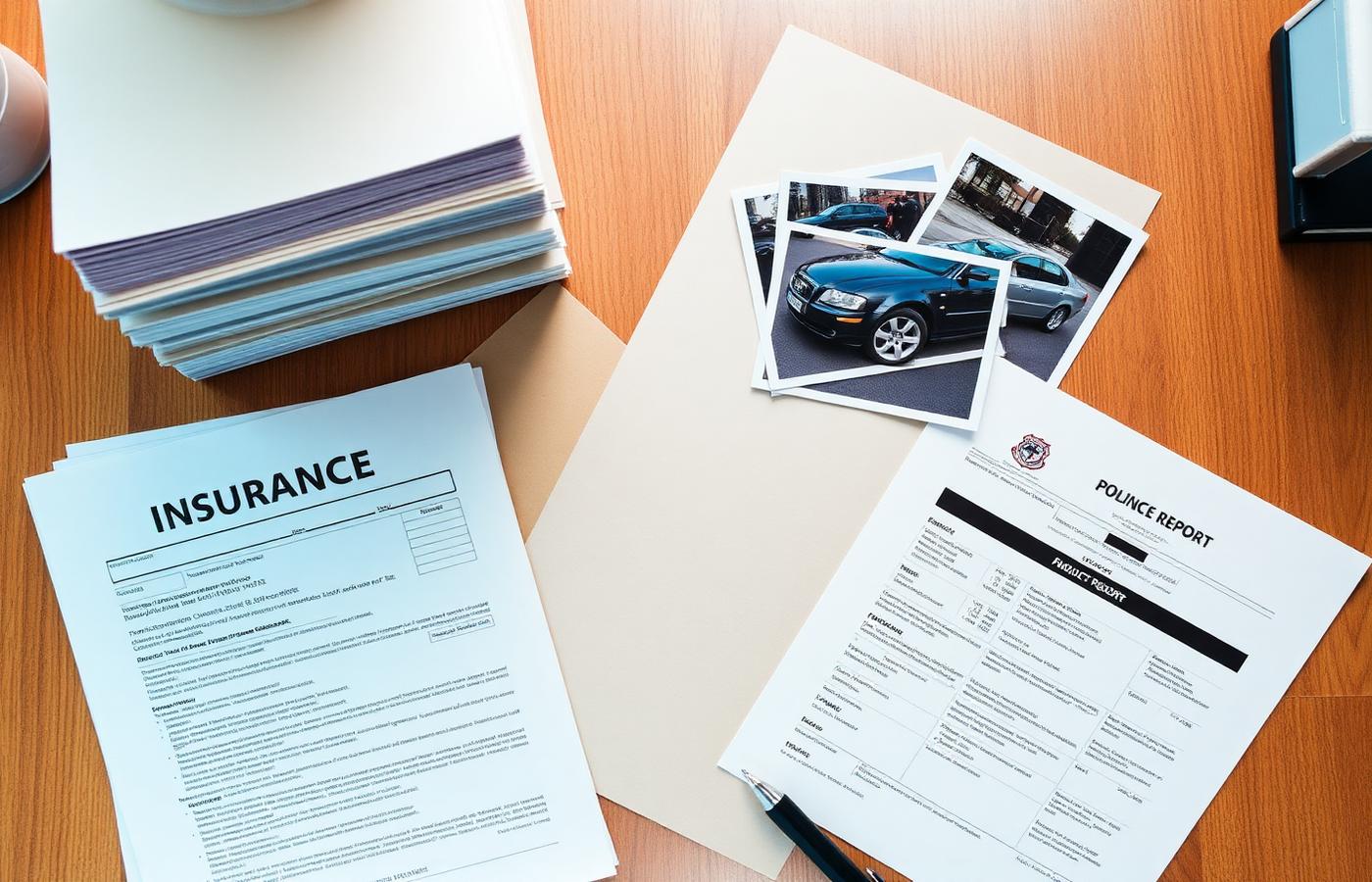

Step 3 — Gather Additional Evidence

Many claim denials are based on insufficient documentation. Strengthening your evidence file can make a decisive difference in your appeal.

Medical Documentation

Obtain complete medical records documenting all injuries, treatments, and diagnoses related to the accident. If your doctor has not yet provided a written opinion connecting your injuries directly to the accident, request one.

Accident Scene Evidence

If you have not already done so, obtain any available surveillance footage, dashcam recordings, or traffic camera footage from the accident scene. Contact businesses near the accident location to request their camera footage before it is deleted.

Witness Statements

Written statements from witnesses who saw the accident can be powerful evidence in an appeal, particularly when liability is disputed.

Independent Repair Estimates

If your claim was denied or reduced based on the insurance company's damage assessment, get independent repair estimates from licensed body shops. A significant difference between their estimate and yours strengthens your appeal.

Expert Opinions

For complex cases involving disputed liability or serious injuries, expert opinions from accident reconstruction specialists or medical professionals can significantly strengthen your appeal.

Step 4 — Write a Formal Appeal Letter

Your appeal letter is your opportunity to make your case directly to the insurance company. A well-written, professional appeal letter significantly increases your chances of a successful outcome.

Your appeal letter should include:

- Opening Statement. Clearly state that you are formally appealing the denial of your claim. Include your policy number, claim number, date of the accident, and the date of the denial letter.

- Summary of the Accident. Provide a clear, factual summary of what happened. Stick to the facts and avoid emotional language.

- Point by Point Rebuttal. Address every reason given for the denial directly. For each reason, explain why you believe it is incorrect and provide the specific evidence that supports your position.

- Reference to Policy Language. If the denial misapplied your policy language, quote the relevant policy provisions directly and explain how they apply to your situation.

- List of Supporting Documents. Clearly list every document you are including with your appeal — medical records, photographs, witness statements, repair estimates, and any other evidence.

- Clear Request. State specifically what you are requesting — full payment of your claim, partial payment, or reconsideration of specific aspects of the denial.

- Deadline Acknowledgment. Reference any appeal deadlines mentioned in your denial letter and confirm that your appeal is being submitted within the required timeframe.

Step 5 — Escalate Within the Insurance Company

If your initial appeal to the claims adjuster is unsuccessful, escalate your appeal to a higher level within the insurance company.

Request to speak with or write directly to:

- The claims supervisor or claims manager

- The department head for your type of claim

- The insurance company's internal appeals department

Document every conversation. Note the date, time, name of the person you spoke with, and a summary of what was discussed. Follow up every phone conversation with a written summary sent by email to create a paper trail.

Step 6 — File a Complaint With Your State Insurance Department

Every US state has an insurance regulatory authority — typically called the Department of Insurance or Division of Insurance — that oversees insurance companies operating in the state. Filing a formal complaint with your state insurance department is a powerful tool that many policyholders do not know they have.

Insurance companies take state department complaints seriously because regulators have the authority to investigate their practices, impose fines, and revoke licenses. The threat of regulatory scrutiny often prompts insurers to reconsider denied claims.

To file a complaint:

- Visit your state's Department of Insurance website

- Submit a formal written complaint with all supporting documentation

- Include the denial letter, your policy, your appeal letter, and all correspondence with the insurance company

Most state insurance departments respond to complaints within 30 to 45 days.

Step 7 — Hire a Car Accident Lawyer

If your appeal is unsuccessful and you believe your claim was wrongfully denied, consulting a car accident lawyer is your next step. An experienced attorney can:

- Review your policy and the denial letter for legal errors

- Identify bad faith insurance practices that may entitle you to additional damages

- File a lawsuit against the insurance company if necessary

- Negotiate directly with senior insurance company representatives

In some states, if an insurance company is found to have acted in bad faith by wrongfully denying a valid claim, you may be entitled to compensation beyond your original claim amount — including legal fees and punitive damages.

What Is Insurance Bad Faith?

Insurance bad faith occurs when an insurance company unreasonably denies a valid claim, delays payment without justification, fails to investigate a claim properly, or offers a settlement that is far below the true value of the claim.

Signs of potential bad faith include:

- Denying your claim without a clear explanation

- Refusing to investigate your claim thoroughly

- Significant delays in processing your claim without explanation

- Making lowball settlement offers with no factual basis

- Misrepresenting your policy coverage to justify a denial

If you believe your insurance company has acted in bad faith, a car accident lawyer can advise you on whether you have grounds for a bad faith lawsuit. Knowing what to say (and not say) to your insurance adjuster from the start helps preserve your case if litigation becomes necessary.

Key Takeaways

- A claim denial is not final — a significant percentage of denied claims are successfully overturned on appeal

- Read your denial letter carefully to understand the exact reason for the denial

- Review your full insurance policy to determine whether the denial correctly applies your coverage

- Gather additional evidence to strengthen your appeal including medical records, witness statements, and independent repair estimates

- Write a formal, professional appeal letter addressing every reason for denial point by point

- Escalate within the insurance company if your initial appeal is unsuccessful

- File a complaint with your state Department of Insurance as a powerful free tool

- Consult a car accident lawyer if the denial appears to be wrongful or made in bad faith

Conclusion

A denied car insurance claim is frustrating, but it is far from the end of your options. Insurance companies make mistakes, misapply policy language, and sometimes deny valid claims hoping policyholders will simply give up.

Do not give up.

By understanding the reason for your denial, gathering strong evidence, writing a compelling appeal, and escalating through every available channel, you give yourself a genuine chance of overturning the decision and receiving the compensation you are owed.

And if the insurance company refuses to honor a valid claim even after a thorough appeal, the legal system exists precisely to hold them accountable.

Your policy is a contract. You paid for that coverage. You have every right to fight for it.

Read these related guides on what to say to your insurance adjuster, how much your car accident settlement could be worth, and how much a car accident lawyer costs. Have a question about your denied claim? Send us a tip — we read every email.

Frequently asked questions

How long do I have to appeal a denied car insurance claim?+

Deadlines vary by insurance company and state law. Most policies specify an appeal window of 30 to 180 days from the date of denial. Check your denial letter and policy documents for the specific deadline that applies to your claim. Missing the deadline can permanently waive your right to appeal.

Can I sue my insurance company for denying my claim?+

Yes. If your insurance company wrongfully denied a valid claim, you can file a lawsuit for breach of contract. If the denial was made in bad faith, you may also be able to sue for bad faith damages which can exceed your original claim amount. Consult a car accident lawyer to evaluate your options.

Does filing an appeal affect my insurance rates?+

Filing an appeal for a not-at-fault claim should not directly affect your rates. However, if your appeal leads to a paid claim under a policy where rates are affected by claims history, there may be an indirect effect. Ask your agent specifically about how a successful appeal would affect your premium.

Should I get a lawyer before filing my appeal?+

For straightforward denials based on missing documentation, you may be able to handle the appeal yourself. For complex denials involving disputed liability, policy interpretation disputes, or potential bad faith, consulting a lawyer before filing your appeal will give you the strongest possible position.

Continue reading

Sources

Have you ever filed a car insurance claim?

Share your experience or send us a tip — our reporters read every email and use anonymized stories to shape future coverage.

Send us your storyMore from Crash & Cover

How Much Does a Car Accident Lawyer Cost? The Truth About Contingency Fees

Fear of legal bills stops most accident victims from ever calling a lawyer. Here is the truth about contingency fees — and why hiring an attorney usually costs you nothing upfront.

Daniel Reyes · May 15, 2026 · 11 min

When To Hire a Car Accident Lawyer (and When You Truly Don't Need One)

Not every crash needs an attorney. Here is the honest line — when a car accident lawyer pays for itself, and when you can settle alone.

Hassan Mwangi, J.D. · May 2, 2026 · 13 min

How to Negotiate an Insurance Settlement After a Car Accident — Step by Step Guide

The insurance company's first offer is almost never their best offer. Here is the step-by-step playbook for countering lowball offers and negotiating the settlement you actually deserve.

Daniel Reyes · May 21, 2026 · 16 min